Financial literacy is a crucial ability for individuals to possess in the fast-paced world of today since it enables them to make educated decisions regarding their money. It is essential to have a thorough awareness of the complexities involved in the process of managing your money, regardless of whether you are a recent college graduate, a young professional, or someone who is seeking to regain control of their finances. In this blog post, we’ll discuss the value of having a solid understanding of personal finance and how it may help pave the path toward achieving financial independence.

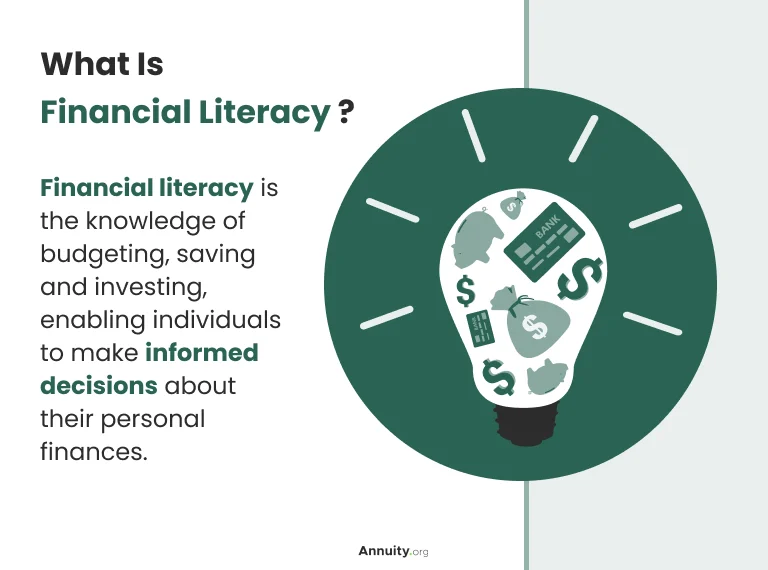

What exactly does the term “financial literacy” mean?

Literacy in finance refers to an individual’s capacity to comprehend and efficiently administer several facets of their personal money. It includes information about things like budgeting, saving, investing, managing debt, and a lot of other things. At its core, it boils down to having the knowledge, experience, and self-assurance necessary to make intelligent judgments regarding one’s finances.

The Numerous Advantages of Having a Good Financial Education

A thorough education in finance may provide you with a number of benefits that can have a substantial influence on your life. It provides you with the information and skills necessary to make educated decisions about a variety of financial matters, including managing your debt, investing, and creating a budget. This empowerment alleviates financial stress, boosts your capacity to achieve both short-term and long-term goals, and lays the groundwork for improved financial stability.

You will be better equipped to face the unforeseen problems that life throws at you, to make intelligent investment choices, and to ensure your retirement security if you have a solid education in finance. It results in increased financial independence, mental tranquility, and the capacity to prosper in an economic environment that is always shifting.

Assessing Your Current Financial Literacy

The assessment of your financial literacy is more than just a test; rather, it is a measurement of both your financial well-being and your level of readiness. Your ability to efficiently manage your investments, as well as your income and spending, will be evaluated. A low score may suggest areas that need development, while a high score indicates a great knowledge of budgeting, saving, and debt management.

Financial literacy may be measured by taking the Financial Literacy Test. Your level of financial literacy is a good indicator of both your ability to make sound decisions and your future financial well-being. Taking the exam will help you identify areas in which you are particularly skilled as well as areas in which you may want further information. This will enable you to make educated decisions regarding your finances and work toward achieving your financial objectives.

Identifying Varied Levels of Knowledge

It is vital to determine the different degrees of knowledge that exist in the field of financial literacy. People may generally be placed anywhere along a spectrum, from a beginner to an expert. Some people may be excellent at financial planning for retirement but have difficulty managing their debt, while others may have a firm grip on financial planning for retirement but struggle to keep their spending under control.

Recognizing these differences is the first step in resolving the gaps in knowledge and developing education that is suited to each person’s specific needs. You will be able to devise a focused strategy for progress after you have determined where you are now on this spectrum. There is not a single approach that can be taken to achieve financial literacy; rather, it is about understanding your own strengths and shortcomings and taking action to close the knowledge gap.

Recognizing what it is that you do not already know is the first step toward filling in the blanks in your knowledge, so you should do that right away. Individuals typically lack competence in a variety of basic areas, including investing, comprehending credit, and planning for retirement.

The Foundations of a Budget

The notion of efficiently allocating one’s money in order to achieve one’s monetary objectives serves as the bedrock upon which a budget is constructed. The first step is to keep detailed records of your income and expenses, which will provide you with an accurate picture of your current financial situation.

Important aspects include classifying expenditures, distinguishing between essentials and luxuries, and establishing financial boundaries for spending. Developing a feasible spending plan that allows for both savings and the settlement of debt is the best way to secure financial security.

It is imperative that the budget be examined on a consistent basis and that any necessary adjustments be made. A well-constructed budget is not just a financial tool but also a route to financial independence since it enables you to manage your resources, minimize your debt, and accomplish both short-term and long-term financial goals.

Acquiring Knowledge About Credit

Learning the ins and outs of one’s credit score is an essential component of becoming financially literate. It requires having an awareness of how credit works and the influence it might have on your own finances. You will get an understanding of credit scores as well as credit reports, both of which play an important part in the process of acquiring loans and negotiating advantageous interest rates.

When applying for credit cards, mortgages, or auto loans, responsible credit management is an absolute must. You will also go through methods that may be used to maintain a favorable credit history, such as making payments on time and keeping your credit utilization under control. A complete education on credit not only gives you the ability to grow and defend your credit score, but it also unlocks the door to better financial prospects and gives you more flexibility with your money.

The Value of Putting Money Aside

It is impossible to stress the importance of developing a savings habit. Having a healthy savings account is essential to having a secure financial future and a prosperous future overall. It serves as a safety net in case of an emergency, reduces the stress that your financial situation is causing, and makes it possible for you to accomplish your goals, such as buying a home, starting a business, or retiring in style.

Your money has the potential to increase in value over time if you invest some of it, and saving gives you the means to do so. Establishing and maintaining regular savings habits is a great way to cultivate discipline and financial responsibility. It is the difference between surviving from paycheck to paycheck and having the flexibility to make decisions that are in line with your long-term goals and aspirations. Saving money is the most important step you can take toward achieving financial stability and the life you desire.

An Overview of the Investing Process

Putting money into investments can help your wealth expand over time. Find out why investing is so important, investigate the many investment opportunities available, such as stocks, bonds, and mutual funds, and make sure you are aware of your comfort level with risk before making investment decisions.

Preparing for Your Retirement

One of the most important and significant financial goals you may pursue is getting ready for retirement. It requires a great deal of forethought and savings for a time in the future when one will no longer be actively employed. When planning for retirement, it is important to establish specific financial objectives, get familiar with the many retirement account alternatives available to you, and make consistent contributions.

It is essential to give thought to investments that increase in value over the course of time in order to guarantee that you will have the financial resources necessary to continue your current lifestyle and follow your hobbies once you retire. Planning ahead of time is beneficial since it enables your assets to grow at a faster rate over time.

Your assurance of financial stability and the key to living your golden years to the fullest may be found in a retirement plan that has been meticulously crafted and implemented.

Debt Management and Types of Debt

Loans and lines of credit used to finance investments that have the potential to boost one’s overall net worth are examples of “good debt.” Some examples of loans are mortgages for purchasing a home, student loans for obtaining an education, and business loans for starting a company. These kinds of debts often have more manageable interest rates and could even come with certain tax advantages.

Bad debt, also known as high-interest consumer debt, includes outstanding amounts on credit cards and payday loans, both of which do not contribute to your overall financial progress and are therefore classified as bad debt. If they are not handled well, they can soon get out of hand and become unmanageable. In order to lessen the impact of financial stress and move closer toward reaching financial independence, effective debt management solutions sometimes entail giving priority to the repayment of bad debt.

A strong foundation for financial literacy may be provided through the formal financial education that is offered in schools and institutions. Examine the benefits and drawbacks of receiving a formal education, and think about enrolling in or pursuing related classes or degrees.

The Best Internet Sources

The information that can be found about finance may be found in abundance on the internet. There are a great number of informative websites, blogs, discussion groups, and online courses available. Make use of these tools so that you can improve your financial literacy without having to leave the comfort of your own home.

Establishing one’s financial Plan

The first thing that one must do in order to ensure that they will have a secure financial future is to create a financial plan. This requires determining specific monetary objectives and developing an all-encompassing strategy for achieving them. It’s important to identify both short-term and long-term goals, such as putting money down for a down payment on a house, college tuition, retirement, or a comfortable lifestyle. Creating a budget, setting aside money for savings and investments, and paying off debt should all be included in your financial strategy. It is essential to revisit your strategy on a consistent basis and make necessary adjustments when new aspects of your life emerge. You may gain control over your money, lessen the stress associated with your finances, and ensure that your financial resources are aligned with your ambitions if you engage in financial planning. In the end, it serves as a guide to achieving financial independence and

Developing a Strategy for Your Finances

Creating a plan for how you will manage your money is essential to having successful financial outcomes. It requires establishing crystal-clear financial objectives, whether for the short term or the long term, and developing a strategy to accomplish those objectives. Managing debt, creating a budget, saving money, and investing are all components of this method.

To do so requires an assessment of your existing financial status, an evaluation of your comfort level with risk, and ongoing monitoring and modification of your strategy in accordance with changing circumstances. A carefully crafted financial strategy not only gives you the ability to make educated decisions regarding your finances, but it also brings your financial resources in line with the goals that you have set for yourself.

It is your road map to achieving financial stability and autonomy, guaranteeing that the money you have worked so hard to obtain will work for you rather than the other way around.

Crucial Moments in One’s Life

Moments of significance in a person’s life are turning points that can have a significant influence on their financial well-being. They include things like getting married, having children, purchasing a home, and eventually reaching retirement age. These life events come with major monetary repercussions, whether it is the management of shared funds after marriage or the preparation of a college fund for a kid.

Both purchasing a home and funding one’s retirement require significant financial commitments in the form of loans and investments, respectively. These crossroads may also bring difficulties, such as the dissolution of a marriage or a slump in the economy. It is crucial to have adequate financial knowledge and preparation before experiencing these significant life events.

In order to maintain financial stability and prosperity during and beyond these critical occasions, it is necessary to make decisions based on accurate information and to plan finances using a strategic approach.

Crises and Deteriorating Economic Conditions

Unexpected crises or economic downturns may jeopardize your ability to maintain a stable financial position. Investigate the significance of keeping reserves for unexpected expenses and educate yourself on the many support programs offered by the government that might bring comfort in times of adversity.

Educating Children About Financial Matters

Teaching children about money and budgeting is a duty that should not be taken lightly. Beginning when they are young, it is necessary to instruct kids on the fundamental ideas of money, including saving, budgeting, and appropriate spending. Kids get a sense of the worth of money and learn how to make educated decisions about their finances when they are taught financial literacy. A culture of frugality and the establishment of goals may be cultivated through the practice of encouraging savings, whether through allowances or piggy banks.

These early lessons in financial responsibility establish the framework for a safe financial future, helping children avoid common financial mistakes and making it easier for them to make educated decisions as they mature into people who are knowledgeable about managing their finances. This is an investment in their long-term independence and financial well-being, and financially speaking.

Programs for the Financial Education of Young People

It is essential to provide today’s youth with the knowledge and tools necessary to successfully navigate the treacherous waters of the complicated world of personal finance, which is why programs designed specifically for this purpose are so important. These programs may be found in schools, community organizations, and online platforms, and they offer classes, workshops, and materials that are specifically geared toward different age groups.

They go through things like developing a spending plan, saving money, understanding credit, and investing. By teaching these essential skills at a young age, financial education programs equip young people with the ability to make well-informed decisions, properly manage their finances, and establish a strong foundation for their monetary future. This is an investment in their economic freedom and long-term financial prosperity.

The Changing Nature of the Financial Landscape

The ever-shifting character of the financial environment is a reflection of the developing economic tendencies, technological advances, and shopping practices of modern consumers. The way that we handle our financial matters has been significantly reworked as a result of developments in fintech, digital payment systems, and decentralized financial systems. Innovations like robot advisors and cryptocurrency have rendered traditional methods of investing obsolete.

The globalization of the economy and the growing accessibility of global marketplaces both bring up new opportunities and threats. The gig economy and remote labour have an impact on both income sources and the methods of financial planning. To successfully adapt to this ever-changing environment, it is necessary to engage in ongoing education, maintain a high level of awareness, and make financially responsible choices. In the ever-changing world

Learning Without Stopping

Learn Without Stopping is a motto that captures the spirit of continuous learning throughout one’s life, particularly in the field of financial literacy. The landscape of personal finance is ever-shifting, giving rise to both new possibilities and obstacles at each stage of development. To be successful in an ever-changing world, it is essential to cultivate a mindset that prioritizes lifelong education. This necessitates maintaining an attitude that is receptive to novel concepts, being current on the ever-shifting trends in the financial sector, and actively seeking out new possibilities to increase one’s financial literacy. The pursuit of information, whether it be through books, classes, internet resources, or financial news, is the instrument you need to adapt, make educated decisions, and create a financially bright future for yourself. Therefore, never stop learning, expanding, and developing your skills.

In Conclusion!

A solid understanding of personal finance may serve as the compass that points the way to financial independence and stability. You will be more equipped to make intelligent decisions regarding your finances if you become proficient in areas such as budgeting, saving, investing, and managing debt. With this information, you will be able to open doors leading to crucial milestones in your life, such as homeownership and retirement. In this always shifting terrain of the financial world, having access to resources, continuing one’s education, and maintaining a high level of awareness are all essential. Keep in mind that becoming financially literate is a continual process as you listen to inspiring tales and tackle the obstacles that life throws at you. Get the skills necessary to empower yourself, seize control of your financial future, and plot a route that will lead to long-term wealth and mental ease.